Private Credit Crisis Deepens as Defaults Surge and Redemptions Freeze

The private credit markets are doing their utmost best to remind experienced investors of the subprime crisis that preceded the Great Financial Crisis. The contagion seems to be spreading. Private credit fund investors can be forgiven for playing this specific passage from the Hotel California by the Eagles in their heads over the past few weeks. This is as major private credit funds have put notable gates on redemption requests.

Every week the news feels like it is getting worse for private credit funds and their investors. These are just some of the headlines from CNBC this week on the increasing travails in this space. A $14 billion private credit fund run by KKR & Co. and Future Standard was downgraded to Junk by Moody's. The ratings agency noted that non-accrual loans had amounted to 5.5% of Future Standard's loan book. One of the highest levels in the Business Development Company, or BDC, sector. The fund was also cited for a lower percentage of first-lien loans than its peers.

Jeffrey Gundlach, A.K.A the 'Bond King,' noted on CNBC recently. Among the many points the famed billionaire bond investor made was that the current environment was reminding him in some ways of the lead-up to the Great Financial Crisis. Specifically, 'asset prices looked elevated, and initial signs of trouble in certain lending markets were downplayed as isolated incidents.' He also made several observations about the current private credit markets.

'Gating' has entered the investor lexicon since private credit redemption problems first cropped up at Blue Owl Capital in the second half of February. Since then, well-known names like Blackstone and Morgan Stanley have capped redemptions at less than what was requested. Lesser-known names like Stone Asset Management and Cliffwater (at its $33 billion private credit fund) have done the same. This week they were joined by Apollo Global Management and Ares Management Corporation; both funds will allow roughly 45% of overall redemption requests this quarter.

Some terms that were very persistent into and during the Great Financial Crisis are starting to resurface in the commentary around private credit in recent weeks. These include 'price discovery' and 'mark to market.' This should give long-term investors a bit of Deja vu. And there is a new trend sweeping over the private credit and BDC space. That is the increasing use of payment in kind, or PIK.

This is where the lender just adds the interest from a non-accrual loan to the back end of the loan. This allows the debtor to keep current, even as they are not making their regular loan payment. The lender can benefit via a higher non-cash interest rate, provided the debtor eventually makes good. Something very similar was taking place in the FHA mortgage sector due to Covid-related programs for nearly four years. These programs were finally ended for the most part last summer. FHA mortgage delinquency rates were just above 11.5% in Q4, it should be noted. The elevated use of PIK was one reason Moody's downgraded the KKR/Future Standard fund as well.

There are several things prudent investors should keep an eye on in the months ahead. Will more private credit funds gate redemption requests? Will there be even more redemption requests in the coming quarter? Some funds saw over 11% of money being demanded back and gave five percent back this quarter. This can't be doing anything good for investors' confidence in those funds or in the private credit space overall.

I would also keep an eye on the stocks of some of the main players in this space, such as Blue Owl, Blackstone, and Apollo Global Management. They have already been shellacked in recent months, with Blue Owl down some 60% from its highs last spring. If these stocks continue to sell off, it is a harbinger that things are getting worse in this part of the credit markets.

Morgan Stanley recently projected that default rates in private credit direct lending could surge to 8%. This would be well above their 2-2.5% historical average. UBS recently stated the private credit default rate could reach 15% in their worst-case scenario. Far higher than the peak of the financial crisis, it should be noted.

In addition, I would monitor to see if price discovery starts to take place in the private credit space. If some defaulted loans get 'marked to market,' investors should have a better idea of what kind of potential 'haircuts' there will be within these loans. Right now, we are mostly seeing 'extend & pretend' behavior from lenders, including increasing use of PIK as previously noted.

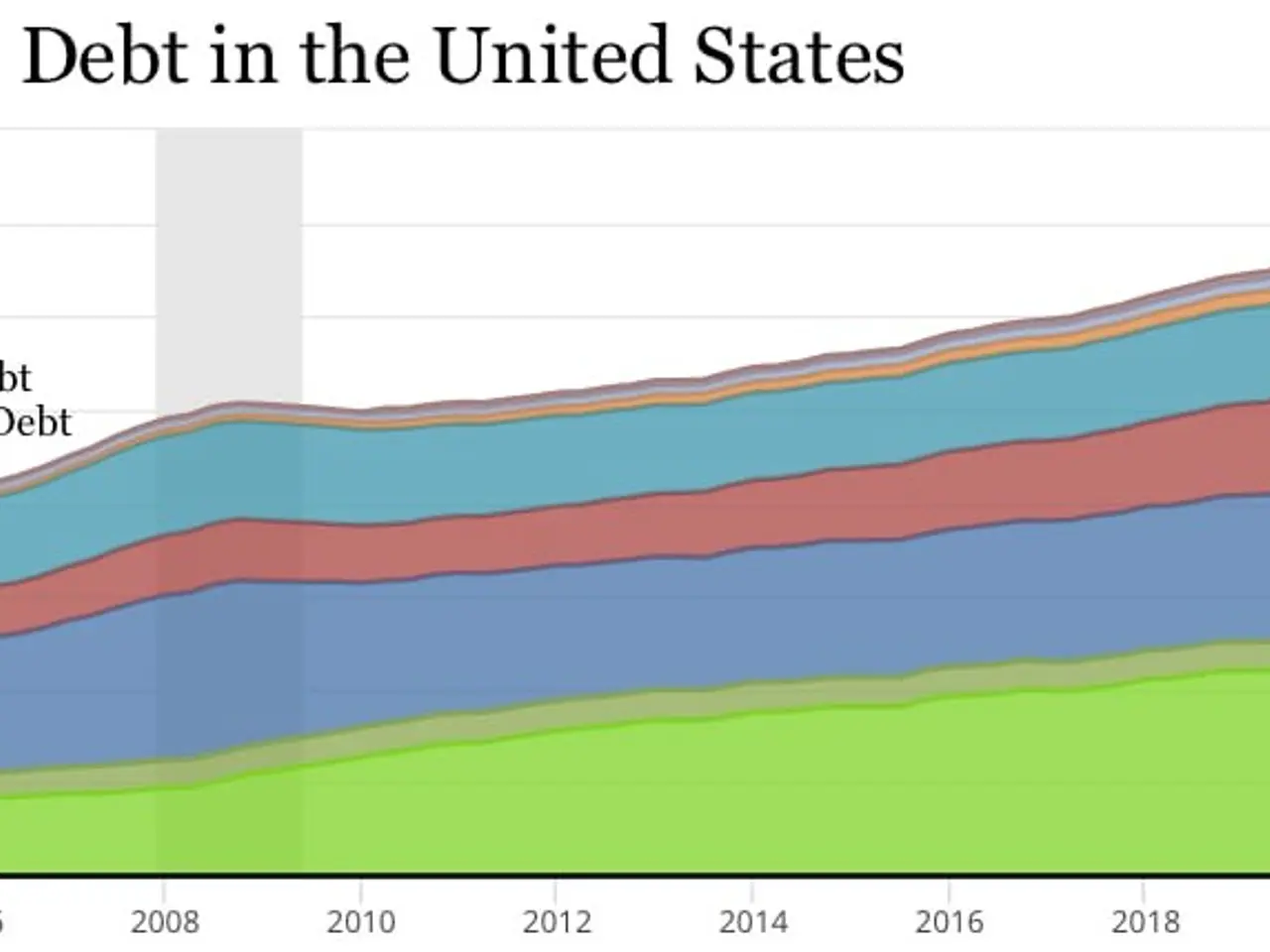

Importantly, I would keep an eye on potential contagion where problems from private credit portend other credit is in trouble. I would particularly keep an eye on commercial real estate, where some $5 trillion in debt is outstanding. Lenders have been engaging in 'extend and pretend,' AKA loan modifications around debt connected to office properties, for some time. Even with that, CMBS delinquency rates for this CRE sub-sector are higher than the peak of the Great Financial Crisis. CMBS delinquency rates against multi-family properties have roughly doubled over the past five quarters. Office and multifamily represent roughly $3.5 trillion of overall CRE debt outstanding.

Investors should keep their eye on apartment REITs like AvalonBay Communities, Inc. to see if their stocks continue to decline as rent growth has slowed down substantially and gone negative in many major regions like Austin, TX.

I would also watch the action in large office REITs like BXP, Inc. and Vornado Realty Trust, whose stocks have staged substantial declines since their highs late last summer. Finally, the health of the regional banking system bears watching. This means keeping an eye on regional banks with large exposures to commercial real estate in their loan books, such as Bank OZK and Flagstar Bank, even as the latter has reduced its exposure to CRE in recent years.

And that is my 'focus list,' as private credit feels more and more like 'Hotel California.' How events play out in the part of the credit markets could well determine which way the equity markets and U.S. economy head in the months ahead.

Read also:

- Peptide YY (PYY): Exploring its Role in Appetite Suppression, Intestinal Health, and Cognitive Links

- Toddler Health: Rotavirus Signs, Origins, and Potential Complications

- Digestive issues and heart discomfort: Root causes and associated health conditions

- House Infernos: Deadly Hazards Surpassing the Flames

{kind=link}